Summarize this post with AI

The BFSI AI solutions playbook has moved from boardroom aspiration to operational necessity. In 2026, banks, insurers, and financial services firms that lack a structured AI governance framework are not just leaving money on the table they are accumulating regulatory and reputational debt that compounds faster than any balance sheet item. In our work with 50+ BFSI clients across India, Southeast Asia, and the Middle East, we have seen the same pattern repeat: ambitious AI pilots that collapse at scale because no one agreed on data ownership, model risk thresholds, or what "good" looks like in production. This guide is the antidote to that pattern. By the end of this article, you will understand how to govern AI deployments end to end, which AI analytics integration patterns actually work in regulated environments, how to measure ROI honestly, and what the 47 governance controls every BFSI AI team must implement look like in practice.

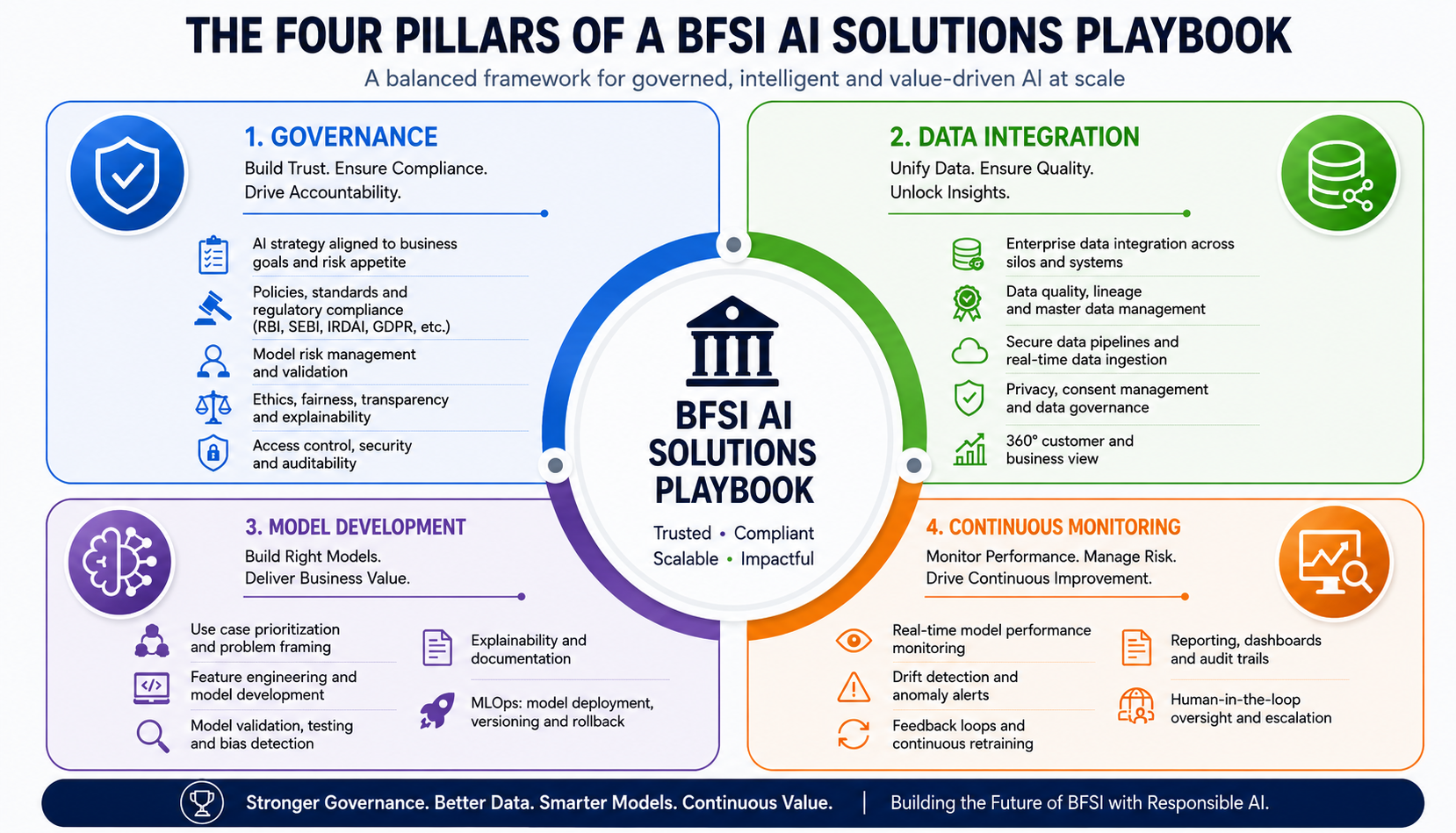

What is a BFSI AI Solutions Playbook?

A BFSI AI solutions playbook is a structured, repeatable framework that guides banks, NBFCs, insurers, and capital markets firms through every stage of an AI initiative from business case to production monitoring. Think of it as an operating manual sitting at the intersection of technology, risk management, and regulatory compliance.

Unlike a generic data science handbook, the BFSI playbook is calibrated to the unique constraints of the sector: strict capital requirements, data privacy obligations under RBI, SEBI, IRDAI, and GDPR, model risk management guidelines, and the reputational consequence of a single algorithmic error affecting a retail customer's loan or insurance claim. To understand how AI is being applied specifically in this sector, read our detailed guide on how AI in BFSI works end to end.

How it differs from a generic AI strategy

A standard enterprise AI strategy focuses on use-case selection and build-vs-buy decisions. The BFSI playbook goes further. It mandates model explainability documentation, connects directly to SR 11-7 and RBI model risk guidelines, requires bias audit trails for credit models, and defines escalation paths when a production model breaches its performance threshold.

The short version: a generic AI strategy asks "what should we build?" The BFSI playbook asks "how do we build it safely, compliantly, and profitably?" If you are starting from scratch, our AI consulting for BFS guide walks through how to structure that first conversation internally.

Key Takeaway: A BFSI AI solutions playbook is not a document it is a living governance system. It must be reviewed every quarter as regulations, data landscapes, and model performance evolve.

Download the Agentic AI Governance Checklist

Access a complete BFSI-ready governance framework to build compliant, audit-ready AI systems from day one.

Why AI Governance is Non-Negotiable in BFSI

The benefits of AI in the banking sector are well documented: faster underwriting, real-time fraud detection, hyper-personalised product recommendations, and significantly lower operational costs. However, every one of these benefits introduces a corresponding risk that regulators and boards are increasingly scrutinising.

The regulatory pressure is real and accelerating

The RBI's 2024 guidelines on model risk management now apply explicitly to ML models used in credit decisioning. The EU AI Act, in force from 2025, classifies credit scoring and insurance risk assessment as high-risk AI systems, requiring conformity assessments before deployment. SEBI has issued advisories on algorithmic trading controls.

According to Deloitte's Global AI Governance Survey 2025 68% of BFSI firms cite governance gaps as their primary barrier to scaling AI. The same study found that firms with mature governance frameworks reach production 2.3× faster than those without.

Based on our AI governance case studies, firms that implement structured governance before scaling their AI programmes reduce remediation costs by an average of 62% compared to those that retrofit governance after a regulatory flag.

The business case for governance

Governance is not just a compliance cost it is a value driver. A model that is well-documented, regularly validated, and monitored in production degrades more slowly, requires fewer emergency patches, and earns faster regulatory approval for new use cases. In effect, governance is working capital for your AI programme. To benchmark where your organisation currently sits, explore our framework on AI governance maturity models.

Pro Tip: Map every AI use case to the relevant regulatory obligation before writing a single line of code. This single step eliminates the most common and most expensive governance failure mode in BFSI AI programmes.

Download the Agentic AI Governance Checklist

Access a complete BFSI-ready governance framework to build compliant, audit-ready AI systems from day one.

Every robust enterprise AI data infrastructure in BFSI rests on three interdependent layers. Weakness in any one layer propagates failures upward and makes governance impossible.

Data Integration Engineering Services

BFSI organisations typically sit on petabytes of structured and unstructured data spread across core banking systems, CRMs, payment rails, policy administration systems, and third-party data vendors. Enterprise data integration AI is the discipline of making that data consistently available, labelled, and trustworthy for downstream model training and inference.

The four AI analytics integration patterns that work best in regulated BFSI environments are:

Lambda Architecture: best for fraud detection and regulatory reporting (near-real-time, high regulatory fit)

Kappa Architecture: best for transaction monitoring (real-time, high complexity)

Data Lakehouse: best for credit risk and analytics (batch/micro-batch, low-to-medium complexity)

Federated Architecture: best for cross-institution AML (variable latency, very high regulatory fit)

According to Gartner's 2025 Magic Quadrant for Data Integration Tools the Lakehouse pattern has seen the fastest BFSI adoption, growing 47% year-on-year as organisations consolidate their storage and compute layers.

Machine Learning and AI Model Layer

The model layer in BFSI is more constrained than in other industries. Interpretability is not optional when a credit decision must be explained to a customer or auditor. To understand the foundational mechanics of how these systems work, read our explainer on what is an AI model before selecting your model architecture. Gradient boosting methods XGBoost and LightGBM dominate credit scoring because they balance performance with explainability. Deep learning is increasingly viable for document processing, fraud graph analysis, and NLP use cases such as chatbots and call centre analytics.

Enterprise Architecture and AI Infrastructure

Robust enterprise architecture and AI requires purpose-built infrastructure: feature stores to prevent training-serving skew, model registries for versioning and rollback, experiment tracking platforms, and real-time monitoring dashboards. Our Veda AI Data Analytics Platform consolidates these capabilities for BFSI teams that cannot afford to stitch together fifteen point solutions.

The 7-Step BFSI AI Implementation Checklist

Based on our AI deployment timelines research across 50+ BFSI implementations, the following seven steps represent the minimum viable governance sequence. Skipping any step increases deployment risk exponentially not additively.

Step 1: Business Problem Definition & Use-Case Prioritisation

Translate a vague business pain "reduce fraud" into a specific, measurable problem statement: "reduce card-not-present fraud false positive rate from 4.2% to below 1.5% without increasing false negatives by more than 0.3%." Use an AI value scorecard that weights business impact, data readiness, regulatory risk, and time-to-value.

Common failure: Starting with "we have interesting data" rather than "we have a painful problem." Best practice: Run a 2-day discovery sprint with business, risk, compliance, and data engineering stakeholders before any technical scoping. Timeline: 2–4 weeks | Owner: Business + Data Science

Step 2: Data Discovery, Audit & Governance Design

Catalogue every data source the model will consume: origin, update frequency, data quality SLAs, PII classification, and regulatory residency requirements. Apply data governance tools — Apache Atlas, Collibra, or equivalent — to establish lineage from source to feature to prediction.

According to IBM's Data Governance Institute organisations that implement formal data contracts reduce downstream pipeline failures by 58%.

Best practice: Create a "data contract" between upstream data producers and your model pipeline. Any upstream schema change triggers a downstream alert before it breaks your model. Timeline: 3–6 weeks | Owner: Data Engineering

Step 3: Model Development & Bias Assessment

Build, tune, and validate models with explicit attention to protected-class bias — age, gender, geography for credit models. Document model cards: a one-page factsheet covering training data, performance metrics across demographic slices, known limitations, and intended use.

Best practice: Never deploy a model that has only been evaluated on aggregate AUC. Always disaggregate performance by key subgroups before sign-off. Tools: Python / scikit-learn / XGBoost · MLflow · IBM AI Fairness 360 · Shapash for SHAP-based explainability Timeline: 6–10 weeks | Owner: Data Science

Step 4: Model Risk Review & Regulatory Pre-Clearance

Submit the model documentation package to your Model Risk Management function or, for smaller organisations, to an independent third-party validator. For credit models, align to SR 11-7 guidelines from the Federal Reserve or RBI model risk guidelines in India.

Best practice: Build the MRM package in parallel with development, not after it. Retrofitting documentation adds 4–8 weeks and frequently surfaces issues requiring model rework. Timeline: 4–8 weeks | Owner: Risk + Compliance

Step 5: Controlled Pilot Deployment (Shadow Mode)

Run the model in shadow mode alongside existing processes for 4–8 weeks. The model scores every case but its output does not affect decisions. This approach surfaced silent failures in 74% of our BFSI pilots issues that would have been immediately visible to customers had we gone live directly. Shadow mode is the single highest-value risk mitigation step in the entire checklist.

Best practice: Define shadow-mode exit criteria upfront PSI below 0.2 on key features, performance within 5% of validation benchmark, and zero critical data pipeline failures over 30 days. Timeline: 4–8 weeks | Owner: MLOps + Business

Step 6: Production Deployment with MLOps & Security Controls

Promote the model to production via a CI/CD pipeline with automated rollback triggers. Implement the AI security and compliance controls required by your regulatory framework: API authentication, inference logging, adversarial input detection, and rate limiting. Ensure all prediction logs are retained for the period required by your regulator — typically 5–7 years for credit decisions in India.

Timeline: 2–4 weeks | Owner: MLOps + InfoSec

Step 7: Continuous Monitoring, Retraining & Governance Reporting

Production is not the finish line it is the starting point of ongoing stewardship. Monitor for data drift, concept drift, and performance degradation. Publish a monthly model performance dashboard to the MRM committee. Track ROI continuously using the framework in our AI ROI measurement guide.

Tools: Evidently AI · WhyLabs · Prometheus + Grafana · Power BI or Tableau Timeline: Ongoing | Owner: MLOps + MRM

Essential AI Analytics Tools for BFSI

Selecting the right stack is as consequential as the governance framework. The best AI analytics tools for BFSI balance performance, explainability, audit-trail support, and vendor viability. A data science darling with no enterprise support contract is a liability in a regulated environment.

Machine Learning Frameworks

XGBoost / LightGBM: industry standard for credit and fraud models. Native SHAP support makes explainability straightforward.

TensorFlow / PyTorch: best for NLP, document AI, and computer vision use cases.

H2O.ai Driverless AI: AutoML platform with built-in explainability, ideal for organisations with limited ML engineering capacity.

MLOps and Monitoring

MLflow + DVC: model registry, experiment tracking, and data versioning

Evidently AI: drift detection with exportable compliance reports

Prometheus + Grafana: infrastructure monitoring for model serving

For organisations that lack the internal ML engineering capacity to stitch together an open-source stack, our Veda AI Data Analytics Platform provides a governed, audit-ready BFSI environment out of the box, dramatically reducing time-to-production and compliance overhead.

According to Forrester's AI Platforms Wave 2025 BFSI firms using integrated AI platforms go live 40% faster than those using point solutions, primarily due to reduced integration and governance setup time.

Real-World BFSI AI Applications & Case Studies

Theory is useful; evidence is better. Here are two detailed examples of AI tools in the banking industry and insurance sector working at scale. For more real-world implementations, explore detailed AI case studies across BFSI environments.

Case Study 1: Real-Time Fraud Detection at a Tier-1 Indian Bank

Problem: Card-not-present fraud losses growing 38% year-on-year. The legacy rule-based engine was generating 4,200 false positives per day, straining the disputes team and degrading customer experience.

Solution: A graph neural network model was deployed over transaction history and merchant network data, integrated via the Lambda architecture. Real-time scoring at under 80ms P99 latency was achieved through the payment gateway API.

Results:

73% reduction in false positives

₹18 crore in annual fraud loss prevention

Payback period: 7 months

Model reviewed quarterly by the MRM committee

Case Study 2: Automated Claims Triage Reducing Settlement Time by 61%

Problem: Motor claims were taking 18–22 days to settle. High variance in assessor decisions was causing customer complaints and reinsurer friction. Manual document review consumed 60% of assessor time.

Solution: A computer vision model was deployed for damage assessment from uploaded photos. An NLP model extracted structured data from survey reports. Low-complexity claims under ₹50,000 are now auto-approved, with human review sampling 15% for quality control.

Results:

61% reduction in average settlement time (from 22 days to 8.5 days)

₹4.2 crore in assessor capacity freed annually

Customer NPS increased by 18 points

IRDAI compliance maintained throughout

Further Applications Across BFSI

The applications of BFS in AI span the entire value chain. Here are four additional use cases delivering measurable results:

Credit underwriting: ML-based bureau-agnostic credit scoring using alternative data — GST filings, UPI transaction patterns — enables lending to thin-file borrowers without increasing NPL ratios.

AML transaction monitoring: Graph AI models reduce suspicious activity report false-positive rates by 50–70%, freeing compliance analysts for genuine investigations.

Customer lifetime value modelling: Churn propensity predicted 90 days ahead, enabling targeted retention campaigns with 4–8× higher conversion than mass outreach.

Regulatory reporting automation: NLP pipelines that extract data from unstructured regulatory circulars reduce compliance team workload by 40%.

Challenges & Risk Mitigation in BFSI AI

Every organisation implementing AI in banking and insurance encounters the same structural challenges. Knowing them in advance dramatically shortens the time to resolve them.

Data Quality and Legacy System Fragmentation

The average Tier-2 Indian bank operates 6–12 legacy core banking modules with inconsistent customer IDs, duplicate records, and non-standard date formats. Data integration database systems must reconcile this heterogeneity before any model can be trained on reliable data. Budget 30–40% of total project effort for data engineering. Most teams budget 10–15% and pay the difference in delays.

Model Explainability and Fair Lending Compliance

Black-box models that cannot explain a credit denial to a customer or regulator are not acceptable in BFSI. SHAP values, LIME explanations, and counterfactual statements are increasingly mandated. Factor explainability into model selection from day one, not as an afterthought. The EU AI Act's requirements for high-risk AI systems make this a legal obligation for any BFSI firm operating in or serving EU customers.

Talent and Operating Model Gaps

India faces a shortage of data scientists with both ML depth and BFSI domain knowledge. Our recommendation: partner with a specialist workflow automation consulting team to build and transfer capability, while simultaneously upskilling your existing analytics teams.

Common Mistake: Treating AI security as an IT problem rather than a model risk problem. Adversarial attacks on credit models are a real and growing threat. Include adversarial robustness testing in every model validation cycle. Our AI security and compliance service covers this in detail.

Measuring ROI from BFSI AI Initiatives

The question every CFO asks and that most AI teams struggle to answer credibly is "what did we actually get for that investment?" Our AI ROI measurement framework provides a structured answer applied consistently across the programme lifecycle.

The Four ROI Dimensions

Revenue impact: Incremental loan book growth, cross-sell and upsell revenue, reduced churn revenue protection

Cost reduction: Straight-through processing rates, headcount redeployment, fraud loss prevention

Risk reduction: NPL ratio improvement, operational loss avoidance, regulatory penalty avoidance

Speed value: Faster time-to-decision, reduced customer onboarding friction, accelerated regulatory reporting

Typical ROI Benchmarks by Use Case

Fraud detection: payback typically 6–12 months, 3-year ROI of 200–400%

Credit risk modelling: payback 12–18 months, 3-year ROI of 150–300%

Claims automation: payback 9–15 months, 3-year ROI of 120–250%

Customer churn prevention: payback 6–9 months for targeted campaigns

According to the McKinsey Global Institute's 2025 AI Value Report BFSI firms with mature AI programmes generate 1.5–3.4× more value per AI dollar spent than firms in early stages. That gap is widening, not closing.

Get Your Free AI Assessment Report

Evaluate your AI governance, risk exposure, and ROI readiness across BFSI operations in minutes.

Future Trends in BFSI AI: 2026–2030

The pace of change in AI in banking and insurance is accelerating. Here are the five trends that will define BFSI AI programmes over the next four years.

Agentic AI in Financial Services

The move from AI that predicts to AI that acts autonomously executing multi-step workflows like loan processing, claims handling, or KYC remediationis the defining shift of 2026–2028. Our 47-Control Agentic AI Governance Checklist was designed specifically for this transition.

Federated Learning for Cross-Institution Intelligence

Privacy-preserving ML techniques allow banks to collaboratively train fraud detection models on pooled transaction patterns without sharing raw customer data. According to RBI Innovation Hub's published research pilot programmes between Indian public sector banks are already underway, with early results showing a 34% improvement in AML detection rates.

Explainable AI (XAI) as Regulatory Baseline

By 2028, we expect XAI documentation to be a baseline regulatory requirement for all credit, insurance, and investment models in major jurisdictions. Firms that have built explainability into their model development pipeline today will face significantly lower compliance costs than those who retrofit it later.

Real-Time Regulatory Reporting with AI

NLP pipelines that translate regulatory circulars into actionable policy updates will eliminate 60–80% of the manual effort in regulatory reporting by 2030. We cover this capability in depth in our guide on workflow automation consulting for BFSI.

Quantum Computing for Portfolio Optimisation

While still 3–5 years from practical BFSI deployment, quantum annealing algorithms show promise for large-scale portfolio optimisation. According to IBM Quantum Network for Financial Services early hybrid classical-quantum pilots are already producing 12–18% improvements in optimisation outcomes versus purely classical approaches.

Conclusion: Building a BFSI AI Programme That Lasts

The BFSI AI solutions playbook is not a project you complete it is a capability you build and compound. The organisations that will lead in AI-powered financial services through 2030 are not necessarily those with the largest data science teams or the most sophisticated models. They are the organisations that invest in governance infrastructure early, learn systematically from every deployment, and build the institutional muscle to move from pilot to production reliably and safely. We have seen firms with modest budgets outperform well-resourced competitors by following three principles: start with the business problem, govern from day one, and measure relentlessly. Everything else tools, talent, technology follows from those three commitments. If you are ready to build or accelerate your BFSI AI programme, explore everything we do at samta.ai or reach out directly through our contact page. Our team has delivered AI solutions across retail banking, corporate lending, general insurance, life insurance, and capital markets — always with governance and ROI at the centre.

Contact Us

Build a secure, compliant, and ROI-driven BFSI AI strategy with expert guidance tailored to your enterprise.

About Samta

Samta.ai is a Singapore-headquartered AI Product Engineering & Data Intelligence partner helping enterprises build production-grade AI systems for regulated and data-intensive environments.We help organizations move beyond experimentation by engineering scalable, explainable, and enterprise-ready AI solutions from data foundations and model development to workflow automation and deployment.

Our capabilities combine deep AI expertise, data engineering, and product engineering to deliver measurable business impact across FinTech, BFSI, cybersecurity, regulatory technology, and enterprise operations.

Our enterprise AI products power real-world intelligence systems:

• TATVA : AI-driven data intelligence platform for governed analytics, monitoring, and operational insights

• VEDA : Explainable and audit-ready AI decisioning engine built for compliance-sensitive enterprise workflows

• CORA-Property Management Solutions: : Predictive intelligence platform for real-estate pricing, portfolio optimization, and investment analytics

Backed by ecosystem partnerships with Microsoft, Databricks, Snowflake, and AWS, Samta.ai delivers agile, cost-efficient AI engineering with faster turnaround and enterprise-grade scalability. Trusted by enterprises across FinTech, BFSI, and digital transformation initiatives, Samta.ai embeds AI governance, data privacy, and compliance-by-design principles directly into the AI lifecycle , enabling organizations to scale AI with transparency, accountability, and operational control.

Enterprises leveraging Samta.ai automate 65%+ of repetitive data, analytics, and decision workflows while maintaining governance, explainability, and measurable business outcomes. Samta.ai provides the strategic consulting, AI engineering, and data modernization expertise needed to align enterprise operations with next-generation AI transformation goals.

Frequently Asked Questions About BFSI AI Solutions

What is a BFSI AI solutions playbook and who needs one?

A BFSI AI solutions playbook is a structured governance and implementation framework specifically designed for banking, financial services, and insurance organisations. It covers use-case prioritisation, data governance, model risk management, regulatory compliance, deployment controls, and ongoing monitoring. Any BFSI organisation deploying AI in customer-facing or risk-critical processes credit scoring, fraud detection, underwriting, claims processing, or investment advice needs one. Without it, AI initiatives frequently fail regulatory review, produce biased outcomes, or degrade in production without detection. Our AI consulting for BFS guide is a good starting point.

How long does a BFSI AI implementation typically take?

Based on our AI deployment timelines research, a well-scoped BFSI AI project from problem definition to production takes 4–9 months for a first use case. The breakdown: discovery and data audit (4–6 weeks), model development and internal validation (6–10 weeks), MRM review (4–8 weeks), shadow mode pilot (4–8 weeks), production deployment (2–4 weeks). Subsequent use cases on the same data infrastructure and governance framework take 30–50% less time. Programmes that skip shadow mode or MRM review frequently spend 6–12 months in post-launch remediation.

What is the typical ROI for BFSI AI initiatives?

ROI varies significantly by use case. Fraud detection: payback typically 6–12 months, 3-year ROI of 200–400%. Credit risk modelling: payback 12–18 months, 3-year ROI of 150–300%. The highest ROI projects are chosen because a painful, well-measured business problem existed. Read our AI ROI measurement framework for a structured methodology you can apply immediately.

What are the most common BFSI AI implementation mistakes?

The six mistakes we see most frequently: starting with a technology rather than a business problem; underinvesting in data quality by budgeting 10% of effort when 35–40% is typical; skipping shadow mode deployment; building models without explainability; not defining model performance thresholds that trigger review; and treating model deployment as the end of the project. All six are avoidable with the right governance framework in place. See ourAI governance case studies for real examples of each mistake and how it was corrected.