Summarize this post with AI

By late 2025, over 70 percent of financial institutions were utilizing AI at scale, up from 30 percent in 2023, yet most Singapore banks and insurers still treat AI as a collection of disconnected pilots rather than an operating model transformation. AI transformation for BFSI is not a technology upgrade; it is a structural change to how credit decisions are made, how fraud is caught, how claims are processed, and how compliance is documented, all simultaneously, under MAS supervisory scrutiny. This playbook covers the highest-ROI use cases, the MAS governance obligations that apply in 2026, and the sequencing framework Singapore BFSI leaders use to move from pilots to production-grade AI.

AI Transformation for BFSI

AI transformation for BFSI in Singapore requires simultaneous execution across three layers: use case deployment in fraud detection, credit risk, AML, and claims automation; data engineering infrastructure that unifies siloed legacy data into AI-consumable pipelines; and a governance framework aligned to the MAS AI Risk Management Toolkit released 20 March 2026 and the proposed MAS AI Risk Management Guidelines. BCG estimates institutions adopting AI with specialist teams achieve up to 60 percent efficiency gains and 40 percent cost reductions in onboarding, compliance, and settlement. For Singapore-regulated institutions, compliance documentation, explainability, and board-level accountability are now supervisory expectations, not optional governance add-ons.

What AI Transformation for BFSI Actually Covers

AI in banking and insurance is the application of machine learning, natural language processing, computer vision, and decision intelligence to core financial workflows including lending, payments, fraud, KYC, claims processing, and compliance reporting. The distinction between AI adoption and ai transformation banking singapore is the operating model. Adoption means deploying a tool. Transformation means redesigning the workflow, the data infrastructure, and the governance structure around AI outputs so that those outputs drive decisions at scale, not just inform analysts. The primary constraint to scaling AI in BFSI is regulatory compliance including explainability, auditability, privacy controls, and formal model risk governance. This is not a technology problem; it is a governance and data architecture problem that technology alone cannot solve. The BFSI AI solutions and governance guide covers how institutions are resolving this gap in practice.

Why 2026 Is the Inflection Point for Singapore BFSI

Three developments make ai and digital transformation in banking a board-level urgency in Singapore this year, not a technology team initiative.

1. MAS supervisory expectations are now operational. On 20 March 2026, MAS announced the successful conclusion of Phase 2 of Project MindForge, publishing an AI Risk Management Toolkit developed collaboratively by a consortium of 24 leading banks, insurance companies, and capital market firms, providing resources for managing AI risks across traditional AI, generative AI, and emerging agentic AI technologies. These are now the practical standards MAS examiners reference.

2. Financial crime compliance costs are forcing automation. In 2024, financial crime compliance costs US and Canadian institutions over $61 billion annually, and $85 billion in EMEA, with figures increasing for 98 percent of financial institutions. Singapore institutions face the same cost pressure. AI-driven AML and fraud detection is shifting from competitive advantage to cost survival.

3. Agentic AI is reshaping what "scaled AI" means. Gartner predicted that 40 percent of enterprise applications will embed task-specific AI agents by end of 2026, up from under 5 percent in 2025. For BFSI, this means autonomous agents that do not just flag anomalies but act on them within defined guardrails, creating a governance requirement that static model risk frameworks were not built to address. For institutions assessing their current governance maturity against these pressures, the MAS FEAT compliance checklist remains the most operationally useful starting reference, and the Singapore BFSI governance balancing guide covers how institutions navigate the innovation-versus-compliance tension in practice.

Map your current AI portfolio against MAS's 2026 Toolkit requirements. Get Samta.ai's AI Risk Assessment Templates, pre-mapped to MAS FEAT, the Operationalisation Handbook, and model risk governance requirements.

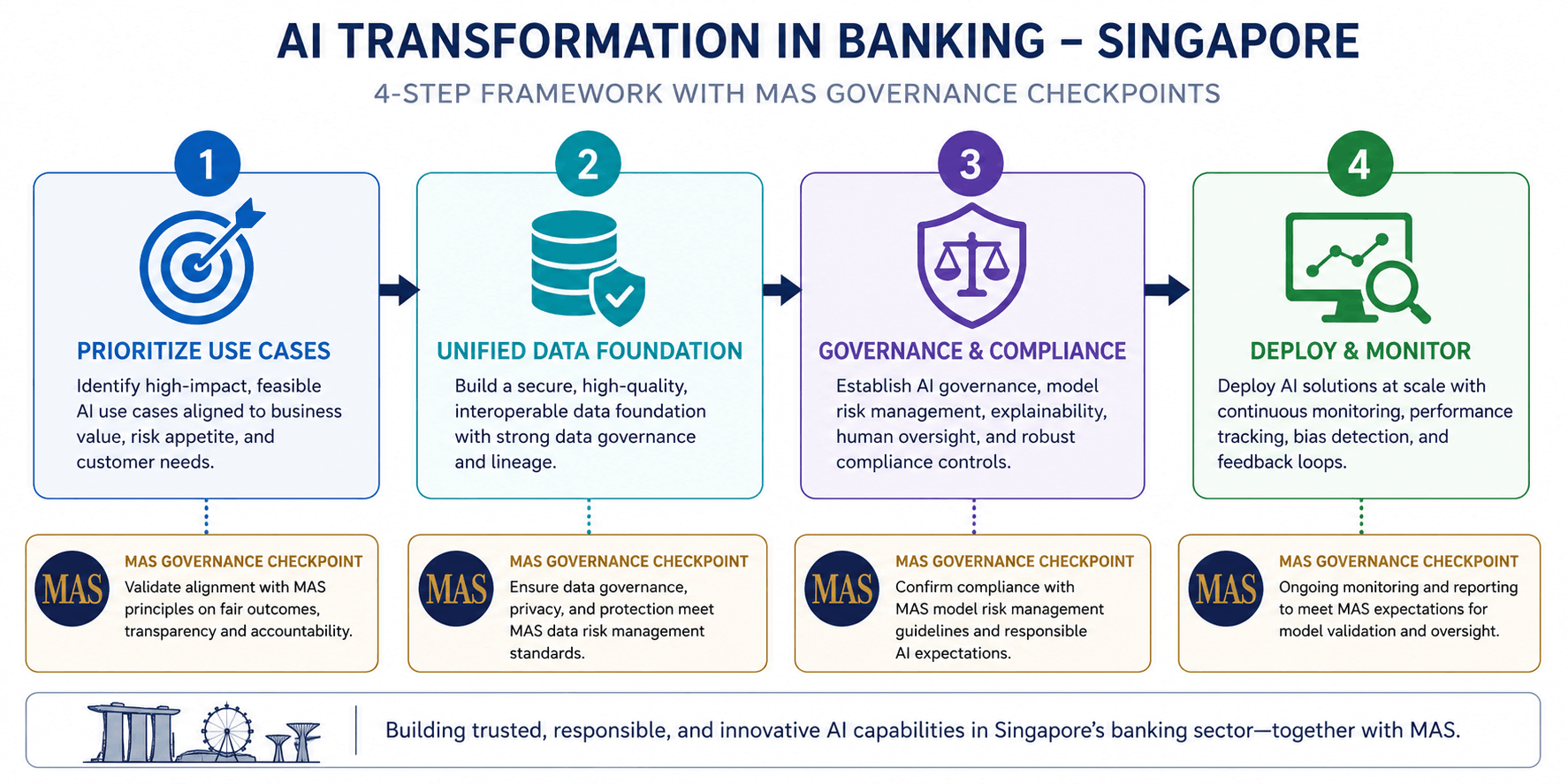

The BFSI AI Transformation Framework: Step by Step

Use this sequence to move from fragmented AI pilots to a governed, production-grade ai business transformation strategy for a Singapore bank or insurer.

Step 1: Prioritize Use Cases by ROI and Data Readiness

The highest-ROI use cases in BFSI cluster around fraud detection, credit risk modeling, AML optimization, intelligent document processing, and operational automation. Score each candidate by business impact, data readiness, integration complexity, and regulatory risk before committing engineering resources. Quick wins come from intelligent document processing and service automation, where data is already clean and regulatory scrutiny is lower. Strategic bets sit in credit, fraud, and AML, where data readiness and regulatory scrutiny are highest but ROI at scale is most significant.

Step 2: Build a Unified Data Foundation Before Model Deployment

Breaking data silos and unifying pipelines is imperative to enable AI agents to work; operating on fragmented data amplifies errors rather than reducing them. Entity resolution across customer, account, device, and merchant data must come before any AI model consumes that data in production. Documentation including data dictionaries, lineage diagrams, and versioning is not good practice; it is the artifact regulators and validators will ask for. Build it before the model, not after.

Step 3: Embed Governance and Compliance from Day One

Compliance teams should be brought in at the time of design, not sign-off. For Singapore-regulated institutions this means MAS FEAT alignment, explainability controls, bias testing documentation, and audit trail architecture all built into the deployment pipeline before a model goes live. MAS's approach is risk-based and proportionate; financial institutions determine the extent to which they adopt requirements depending on the size and nature of their operations, the breadth and depth of their AI applications, and their overall risk exposure. Proportionality does not mean optional; it means calibrated.

Step 4: Deploy and Monitor with Continuous Governance

Samta.ai's Veda AI decision analytics platform supports this step by connecting model inventory, bias detection, drift monitoring, and audit trail generation into a single operational layer across Databricks and Snowflake infrastructure. Rather than maintaining separate governance tooling for each AI system, the Veda AI decision analytics platform provides the continuous monitoring layer that turns MAS Toolkit compliance from a point-in-time exercise into a live operational capability.

Samta.ai's AI security compliance services provide the documentation and audit trail structure that BFSI compliance teams need when MAS examiners request evidence of governance maturity. See how enterprises have applied this in practice via Samta.ai's case studies and complete AI governance guide.

Banking vs Insurance AI Transformation: A Comparison

Dimension | AI in Banking | Insurance AI Transformation | MAS Compliance Layer | Samta.ai Integration Point |

Highest ROI Use Cases | Fraud detection, credit risk modeling, AML optimization | Claims automation, underwriting AI, fraud triage | Model risk documentation, explainability controls | Veda AI decision analytics across both sectors |

Primary Data Challenge | Entity resolution across customer, account, and transaction data | Unstructured claims documents and third party data integration | Data lineage and audit trail requirements | Unified data pipeline on Databricks and Snowflake |

Regulatory Exposure | MAS FEAT, AML Act, credit scoring fairness standards | MAS FEAT, PDPA, actuarial model validation standards | MAS AI Risk Management Toolkit, 20 March 2026 | AI security compliance documentation |

Governance Priority | Board-level model risk ownership, three lines of defense | Independent actuarial and AI model validation | Proportionate risk tiering by impact and complexity | AI risk register and continuous monitoring |

Agentic AI Readiness | Fraud response agents, AML case escalation automation | Claims triage agents, policy renewal automation | ABS Handbook on Generative AI Guardrails in Banking, key input to MindForge Handbook | Agentic AI governance layer via Veda AI |

Enterprise Use Cases: How Singapore BFSI Applies AI Transformation

Use Case 1: Singapore Bank Deploying AI-Driven Fraud Detection

A Singapore bank replaced its rule-based AML transaction monitoring system with an AI-driven anomaly detection model fed by a unified customer entity graph. Traditional rule-based AML systems generate a high number of false positives; AI components added to existing systems enable identification of genuine fraud signals at scale. The bank's governance structure documented every model decision for MAS compliance purposes, with explainability outputs generated automatically for any case escalated to a human investigator. False positive rates dropped by over 60 percent within six months of production deployment, directly reducing the compliance team's workload without reducing detection coverage. For a full breakdown of how AI in banking governance is structured for this type of deployment, see the how AI in BFSI works guide.

Use Case 2: Insurer Automating Claims Processing with AI

A Singapore-based insurer deployed intelligent document processing for claims intake across three product lines. Unstructured claims documents were extracted, classified, and validated against policy data in a cloud data lake, with AI-generated summaries routing cases to adjusters with pre-populated decision support. What is ai in insurance for this insurer meant reducing average claims processing time from four days to under six hours. More importantly, every AI-influenced routing decision was logged with a rationale, giving the compliance team an exportable audit trail consistent with MAS's proportionate governance expectations. The outcome aligned directly with what the how AI is transforming the insurance industry analysis identifies as the highest-value operational AI deployment pattern for APAC insurers.

Key Risks and Failure Modes

Treating governance as Phase 4 work: Compliance teams must be involved at the time of design, not sign-off. Every week of governance retrofit after production deployment costs more than building it in at design stage.

Fragmented data creating fragmented AI: Most AI program failures in BFSI are operational rather than technical, driven by weak data governance, inconsistent labels, integration gaps, and low user trust. The data engineering layer is not supporting infrastructure; it is the primary risk control.

Black-box models in regulated decision contexts: Since compliance is an accountability function, every decision affecting a customer must be explainable, auditable, and defensible; deep learning models are commonly known as black-box owing to their lack of transparency. Institutions deploying opaque models in credit or claims decisions face both regulatory exposure and customer challenge risk.

Shadow AI proliferating outside governance: Lack of use case, data, and model governance was identified by the ABS Handbook as one of the ten top AI risks for banks. Ungoverned AI tools in use across business units create audit exposure the enterprise cannot document or defend.

Get a structured baseline on your current AI portfolio, data readiness, and MAS compliance posture. Request a Free AI Assessment Report from Samta.ai and enter your transformation program knowing exactly where your gaps are.

Decision Framework: Is Your BFSI AI Program Transformation-Ready?

Use cases are scored by ROI, data readiness, and regulatory risk before any build commitment

Entity resolution and data lineage documentation exist before model training begins

Compliance teams are involved in model design, not just post-deployment sign-off

Explainability controls and audit trails are built into deployment pipelines, not added retrospectively

Board-level AI risk accountability is assigned and documented

Agentic AI systems have distinct governance covering autonomous action risk, not just output accuracy

If fewer than four boxes are checked, your ai transformation for bfsi program carries governance risk that MAS examiners are actively looking for in 2026 reviews.

Conclusion

AI transformation for BFSI in Singapore has moved from competitive aspiration to regulatory baseline. With MAS's AI Risk Management Toolkit active, supervisory examinations evaluating AI governance, and agentic AI deployments accelerating across the sector, Singapore banks and insurers that treat governance as a Phase 4 consideration will face the highest compliance exposure precisely when their AI programs are scaling fastest. The institutions that build data, deployment, and governance in parallel will scale with confidence; the rest will retrofit under examination pressure.

Get the complete framework for governed, production-grade AI in Singapore BFSI. Request Samta.ai's AI Model Risk Management Playbook and map your model inventory, risk tiers, and MAS compliance documentation in one structured program.

About Samta

Samta.ai is a Singapore-headquartered AI Product Engineering & Data Intelligence partner helping enterprises build production-grade AI systems for regulated and data-intensive environments.We help organizations move beyond experimentation by engineering scalable, explainable, and enterprise-ready AI solutions from data foundations and model development to workflow automation and deployment.

Our capabilities combine deep AI expertise, data engineering, and product engineering to deliver measurable business impact across FinTech, BFSI, cybersecurity, regulatory technology, and enterprise operations.

Our enterprise AI products power real-world intelligence systems:

• TATVA : AI-driven data intelligence platform for governed analytics, monitoring, and operational insights

• VEDA : Explainable and audit-ready AI decisioning engine built for compliance-sensitive enterprise workflows

• CORA-Property Management Solutions: : Predictive intelligence platform for real-estate pricing, portfolio optimization, and investment analytics

Backed by ecosystem partnerships with Microsoft, Databricks, Snowflake, and AWS, Samta.ai delivers agile, cost-efficient AI engineering with faster turnaround and enterprise-grade scalability. Trusted by enterprises across FinTech, BFSI, and digital transformation initiatives, Samta.ai embeds AI governance, data privacy, and compliance-by-design principles directly into the AI lifecycle , enabling organizations to scale AI with transparency, accountability, and operational control.

Enterprises leveraging Samta.ai automate 65%+ of repetitive data, analytics, and decision workflows while maintaining governance, explainability, and measurable business outcomes. Samta.ai provides the strategic consulting, AI engineering, and data modernization expertise needed to align enterprise operations with next-generation AI transformation goals.

Frequently Asked Questions

What is AI transformation for BFSI and how is it different from general enterprise AI?

AI transformation for BFSI differs from general enterprise AI in regulatory obligation, data sensitivity, and accountability requirements. Every AI-influenced decision in banking or insurance that affects a customer must be explainable, auditable, and defensible under MAS regulations. General enterprise AI rarely faces this level of scrutiny. The governance layer is not optional in BFSI; it is the primary design constraint.

What are the highest ROI AI use cases in banking and insurance in 2026?

The highest ROI AI use cases in BFSI cluster around fraud detection, credit risk modeling, AML optimization, intelligent document processing, and operational automation. For insurance specifically, claims triage and underwriting automation deliver the fastest payback periods. Quick wins typically come from intelligent document processing; strategic value sits in credit, fraud, and AML where data complexity is highest.

How does MAS governance apply to AI transformation in Singapore banks?

MAS's AI Risk Management Toolkit, developed by a consortium of 24 banks, insurers, and capital market firms, provides resources for managing AI risks across traditional AI, generative AI, and agentic AI technologies. It includes the Operationalisation Handbook with practical implementation guidance. MAS's approach is risk-based and proportionate, requiring institutions to calibrate governance to their size, AI breadth, and risk exposure.

What is AI in insurance and how is it transforming claims processing?

What is ai in insurance in operational terms is the application of NLP, computer vision, and predictive models to claims intake, fraud triage, underwriting, and policy renewal. AI extracts and classifies unstructured claims documents, validates them against policy data, and routes cases with pre-populated decision support. How ai is transforming the insurance industry is most visible in claims processing time reductions and fraud detection accuracy improvements, both of which carry direct compliance documentation implications under MAS expectations.

How do Singapore banks manage agentic AI governance under MAS rules?

Governance of agentic AI for BFSI requires clearly defined escalation protocols, automated circuit breakers, and full audit trails for every agent action. The ABS Handbook on Generative AI Guardrails in Banking identified inadequate human oversight and lack of use case, data, and model governance as top risks. Agentic systems require distinct governance addressing autonomous action risk, not just the output accuracy framework used for traditional models.